By Sachin Rajendra — IIT Bombay, ex-LinkedIn (now Microsoft)

Over the four years I spent at LinkedIn, a meaningful chunk of my compensation came in RSUs. I held on to them — partly because I genuinely believed in what the company was building, and partly because, honestly, moving equity is a hassle. There's the myriad fees, the tax questions, the friction of dealing with portals you never quite understand. It's always easier to just... not.

As Microsoft acquired LinkedIn and the stock kept doing well, what started as one line item in my salary had quietly grown into something worth taking seriously. At some point I knew I needed to diversify. Not because I'd lost faith in Microsoft — it was just basic risk hygiene. Having a meaningful chunk of your net worth in a single stock, however good, isn't a strategy.

The usual options felt wrong

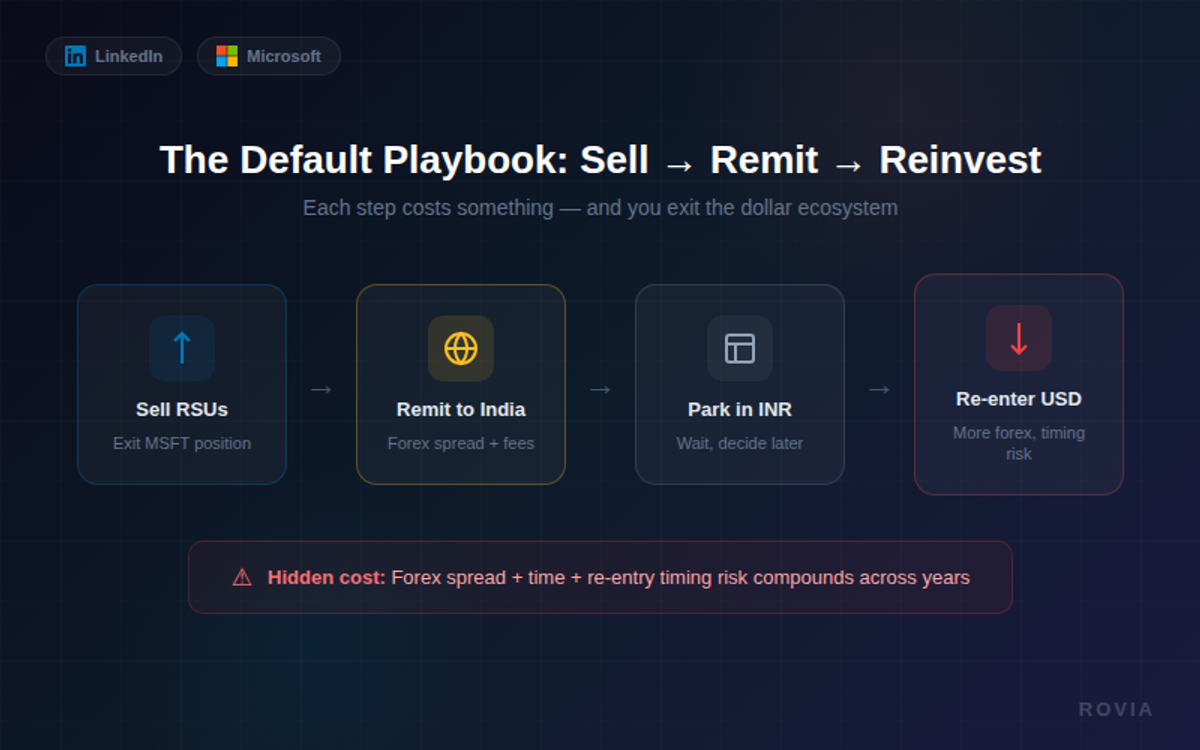

Here's where most of the advice I got fell flat. The default playbook for an Indian professional with US equity is pretty predictable: sell the stock, remit the proceeds to India, deal with the forex conversion, park the money somewhere locally, maybe reinvest after a while.

That logic never quite appealed to me. Each step in that chain costs something — forex spread, time, transaction friction — and more fundamentally, it means you've exited the dollar ecosystem and have to re-enter it later if you want to stay invested globally. I didn't want to do that round-trip. I wanted to diversify within the US market, not evacuate from it.

But the usual options didn't make that easy. Most platforms built for Indian users assume you want the money in India eventually. The whole product architecture is designed around repatriation as the end goal.

A college connection and a different kind of product

Around that time I remembered that Shivang — we go all the way back to college — was building something in this space with Rovia. I reached out to understand what they were doing, and it turned out to be exactly what I was looking for.

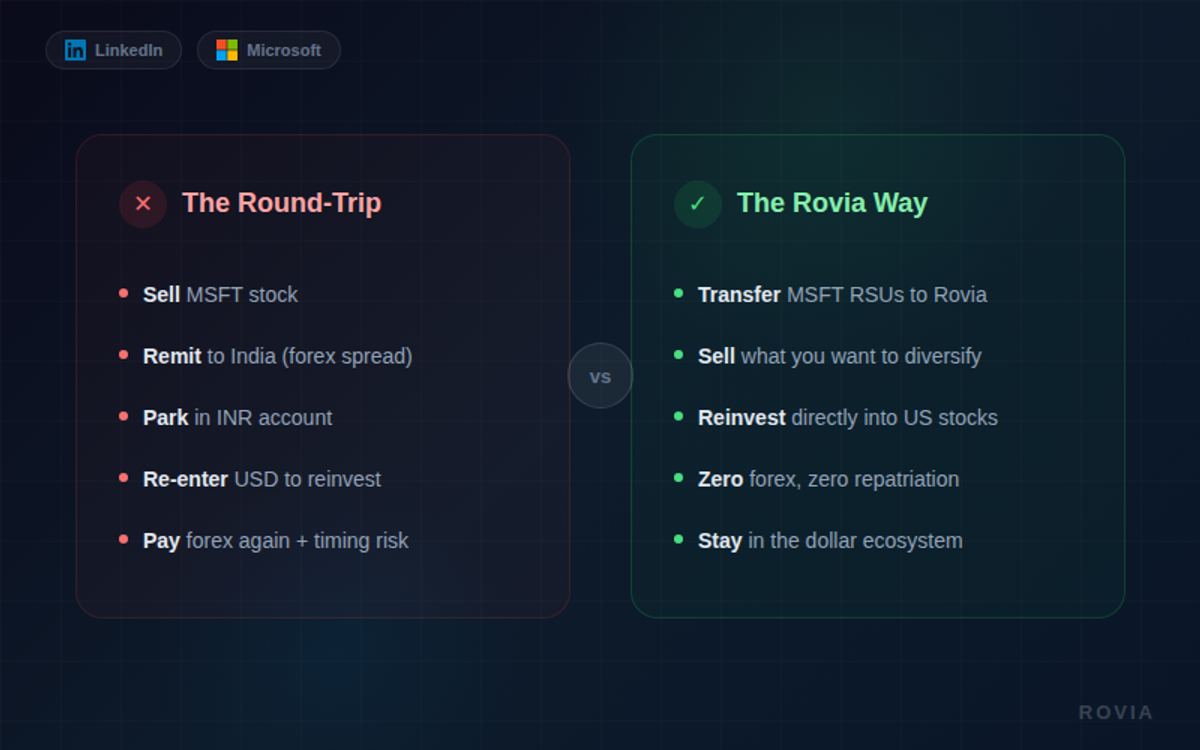

I transferred my Microsoft RSUs to Rovia, sold a part, and reinvested directly into other US stocks — without the usual back-and-forth. No India remittance, no forex leg, no re-entering the market from scratch. The money stayed in the dollar ecosystem and got redeployed. The whole process was pretty straightforward.

One thing I didn't expect: the platform nudged me with some recommendations along the way. Most execution platforms are just that — execution. They process your instruction and stop there. These nudges were different. They actually helped me think more clearly about what I was doing and why. That kind of guided decision-making matters more than people admit when you're dealing with equity you've spent years accumulating.

The philosophy behind the decision

Still early days with Rovia, so I'll stay measured about outcomes. But the decision to try it felt obvious pretty quickly.

For someone like me — who wanted to stay globally invested, diversify within the US market, and avoid the unnecessary movement of money — it was a bit of a no-brainer. The product is doing something most platforms in this space haven't thought to do: letting you act on your US equity without treating India as the default destination for the proceeds.

That's a different product philosophy, and it's one that resonates with how a lot of us actually think about our savings.

If you're sitting on LinkedIn or Microsoft RSUs

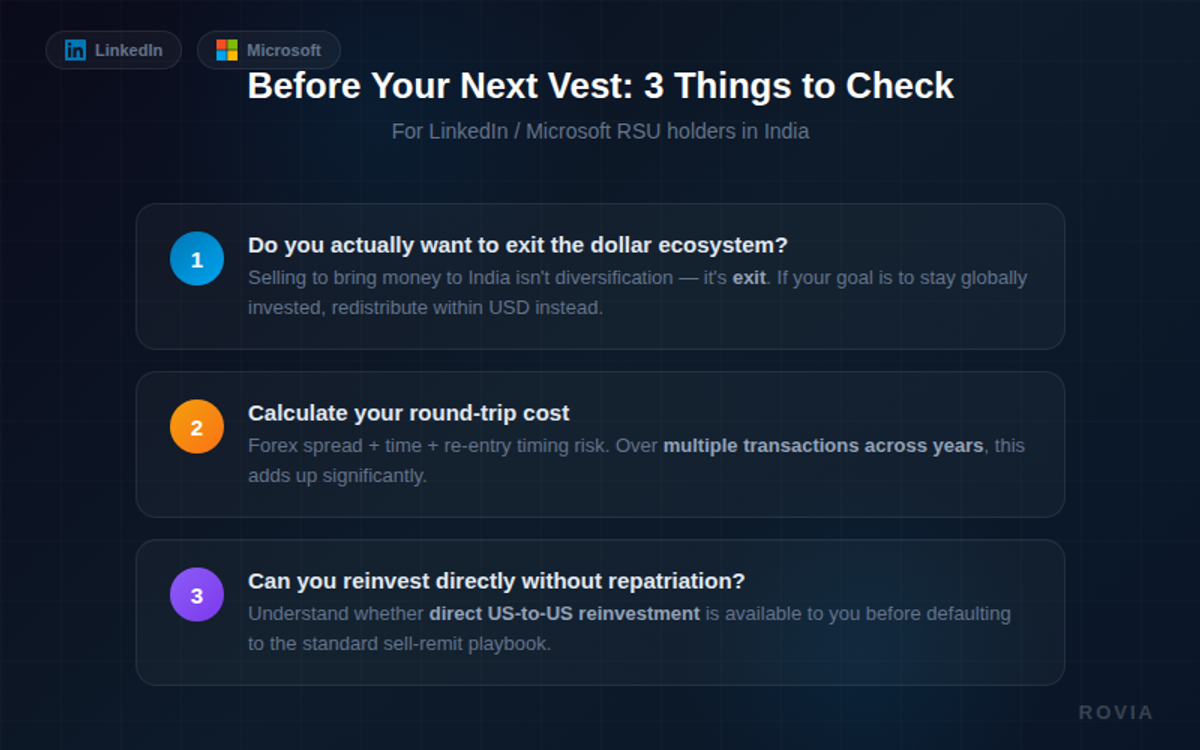

A lot of people from my vintage joined LinkedIn around 2014. Many of them would have accumulated RSUs through the acquisition years, and many of them are probably still holding — out of inertia as much as conviction. If that sounds familiar, a few things worth thinking through:

- ✓If your goal is to stay globally invested, selling to bring the money to India isn't diversification — it's exit. Worth asking whether you actually want to exit the dollar ecosystem or just redistribute within it.

- ✓The round-trip cost of selling → remitting → reinvesting is real. Forex spread, time, re-entry timing risk. Over multiple transactions across years, that adds up.

- ✓If you have the option to reinvest directly into other US positions without repatriation, it's worth understanding whether that's available to you before defaulting to the standard playbook.

Word of mouth counts for something in fintech, especially when the person recommending it built it. For me it started with a college friend who understood the problem from the inside.